Read Articles

View All

Overview of SEBI Regulations for Registrars and Transfer Agents

The SEBI (Registrars to an Issue and Share Transfer Agents) Regulations, 1993 notified on May 31, 1993 have served as one of the important fundamental regulatory framework for the Indian securities market. With the technological developments, the way in which securities are issued, held, and transferred is now fundamentally different. Registrars to an Issue and Share Transfer Agents (RTAs) are key to this process.

Further, the number of securities held in physical form has been going down consistently after the introduction of dematerialization of securities. It may be mentioned that the number of physical shareholding is less than 1% of the total holding as on March 31, 2025. Role of RTAs has further reduced in view of the fact that securities are issued only in dematerialized form.

In response to this changing landscape, SEBI undertook a comprehensive review of RTA regulations, 1993 resulting in notification of SEBI (Registrars to an Issue and Share Transfer Agents) Regulations, 2025 on December 16, 2025.

NISM Study Material

Following is the collection various NISM Study Material of Indian Securities Market. The NISM Study Material may be downloaded from the provided pdfs.

D C Anjaria Committee on Review of SEBI Fee Structure for Stock Brokers

The fee structure for the brokers prescribed in the regulations was based on the recommendations made way back in 1992 by the R S Bhatt Committee. The recommendations of the Committee were based on the then level of brokerage earned by the brokers. Over the next decade, the market structure witnessed sea change, which coupled with fierce competition among brokers, has brought down the level of brokerage drastically. This necessitated a review of the fee structure for the stock brokers. Accordingly, on January 21, 2002, SEBI constituted a Committee under the Chairmanship of Mr. D. C. Anjaria to review the fee structure for the stock brokers. The Committee submitted its report during November 2003.

SEBI - An Evolution of Legislative Empowerment

The article traces the evolution of SEBI from its conceptualization in the G.S. Patel Committee Report, 1985 to its establishment in the year 1988, its empowerment through legislation as a statutory body in the year 1992 and beyond. Accordingly, this article highlights the salient features of Acts such as the SEBI Act, 1992, the Depositories Act, 1996, the Securities Contracts [Regulation] Act, 1956, and the Companies Act, 2013. The article also delves into the details of the important legislative empowerment of SEBI through legislative amendments in the years 1995, 1999, 2002, 2004, 2014, 2015 and 2019.

.png)

Watch Videos

View All

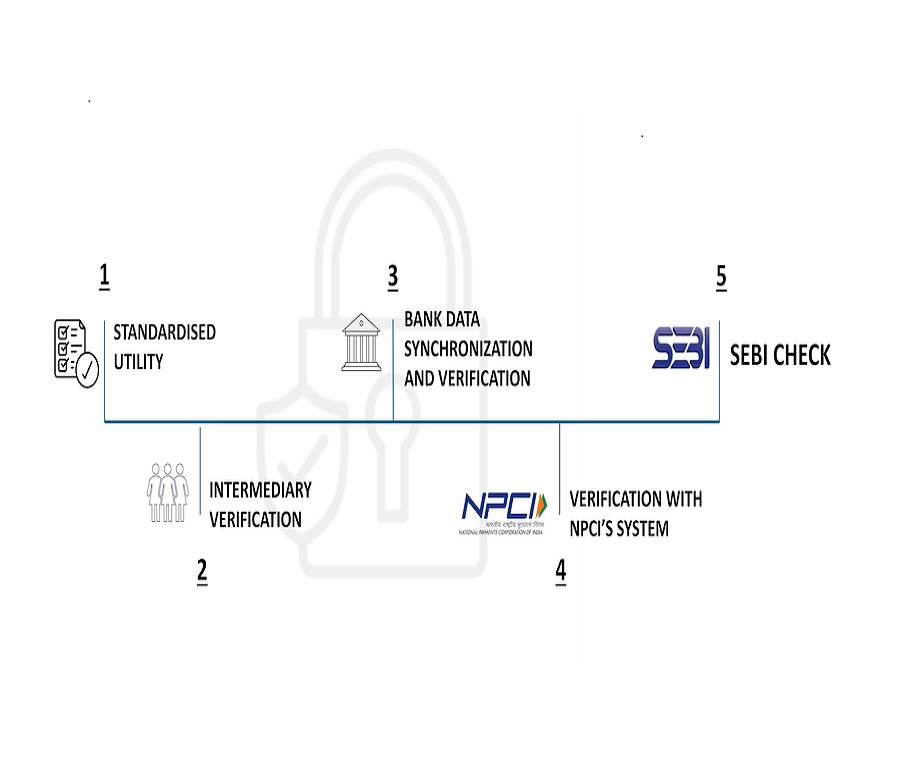

“Validated UPI Handles” and “SEBI Check” for secure investor payments

These two rollouts of “[at]valid Handle” and “SEBI Check” are expected to significantly enhance investor protection by curbing fraudulent money collections by unregistered entities.

Unified Distilled File Formats - UDiFF

SEBI promotes standardised reporting, savings of over Rs. 200 crore over 5 years, 90 percent reduction in reporting requirements for Brokers or Members, lower cost of entry for new fintech.

Pratip Kar - Interview

History comes alive. Watch an interesting discussion of Mr. Pratip Kar, SEBI‘s longest serving Executive Director with Ms. Latha Venkatesh of CNBC.

It is a rare insider‘s account of SEBI‘s origin, its initial struggles, its battles against major market scams, lots of untold stories and a candid take on its landmark successes you don‘t want to miss.

Sundararaman Ramamurthy - Interview

Listen to an in-depth conversation with Mr. Sundararaman Ramamurthy, MD and CEO of BSE, Asia’s first and fastest stock exchange. Established in 1875 as The Native Share and Stock Brokers’ Association, BSE has a rich legacy. This conversation covers a range of topics, from the evolution of stock exchanges to present-day market dynamics, including the role of technology, regulations, and more.

Nehal Vora - Interview

Interview with Shri Nehal Vora, MD and CEO of CDSL: Discover how decades of SEBI-led reforms turned a 19th-century, floor-traded market into a fully digital, AI-enabled ecosystem. Whether you’re an investor, policymaker or fintech enthusiast, this conversation with Shri Nehal Vora charts India’s unique journey from paper to pixels and previews what’s next for inclusive capital-market growth.

SEBI Introduced Validated UPI Handles and SEBI Check

SEBI announced a significant initiative to enhance investor protection and combat unauthorized money collection in the securities market. Effective October 1, 2025, SEBI will introduce a structured and validated UPI address mechanism, featuring the exclusive valid handle, for all SEBI-registered investor-facing intermediaries.

Application Supported by Blocked Amount in Secondary Market

SEBI SMART 2025- A symposium of Indian Securities Market Tech Stack

Central Demise Reporting

SEBI SMART 2025- A symposium of Indian Securities Market Tech Stack

Security and Covenant Monitoring Platform

SEBI SMART 2025- A symposium of Indian Securities Market Tech Stack

Software as a Service

SEBI SMART 2025- A symposium of Indian Securities Market Tech Stack

View Images

View All

Role of financial institutions

Development finance institutions have played a constructive role in establishing India's industrial base. However, these institutions seem to have moved away from their developmental role and are getting entangled deeper in management and control of private sector industries. Corporate circles have been pleading for a re-examination of the role and appointment of nominee directors to avoid day-to-day interference in company operations. Furthermore, some argue that financial institutions should keep their funds rolling by disposing of shares with a ready market. The concept of growth or mutual funds has yet to take root in the country, but such funds could prove successful in mobilising and canalising community savings for industrial development.

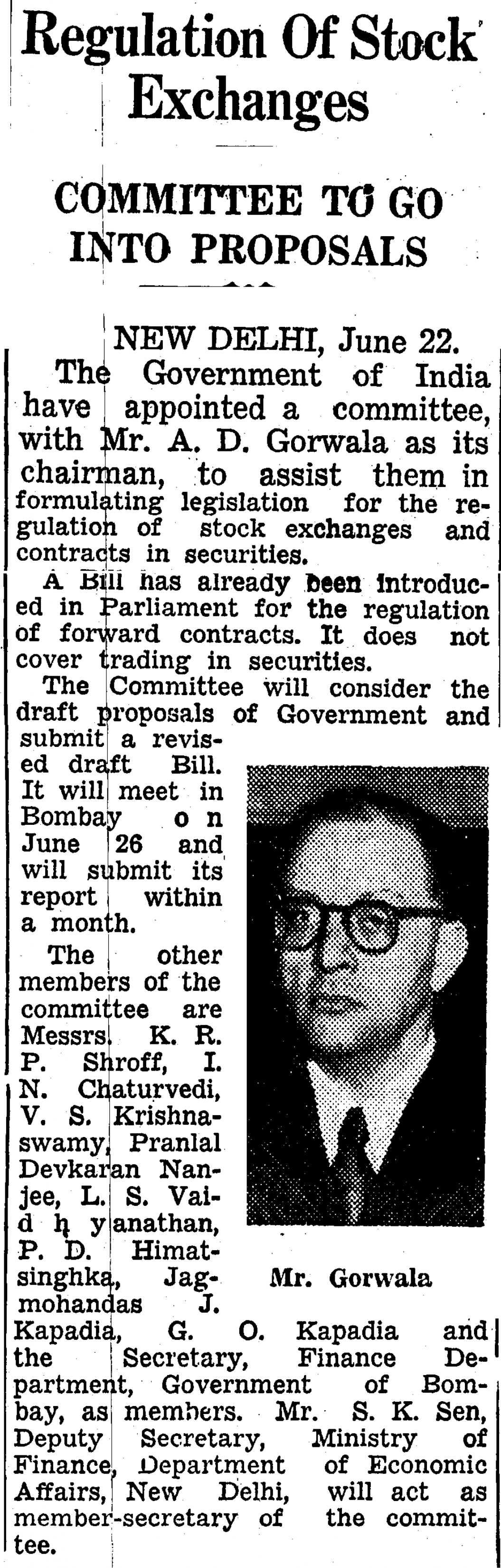

Regulation of Stock Exchanges

The Government of India have appointed a committee, with Mr. A. D. Gorwala as its chairman, to assist them in formulating legislation for the regulation of stock exchanges and contracts in securities. While a Bill has already been introduced in Parliament for the regulation of forward contracts, it does not cover trading in securities. The Committee will consider the draft proposals of Government and submit a revised draft Bill. It will meet in Bombay on June 26 and will submit its report within a month.

Reform Markets

The unrepentant tone of the letter sent by Mr. Harshad Mehta to the CBI focuses attention on reforms urgently needed to make financial markets level playing fields for all. While big operators liquidated positions before prices fell, India lacks laws against such insider trading, allowing operators to take markets sky high with unauthorised bank accommodation. Furthermore, Mr. Mehta accused the Reserve Bank of India of quietly countenancing unconventional practices now called into question. What is now needed is enlightened leadership with the foresight to direct reform along correct lines

Securities contract rules amended

The government has amended the Securities Contracts (Regulation) Rules, 1957, to allow a company to become a member of a stock exchange if it satisfies certain conditions. The conditions are that the company is formed in compliance with the provisions of section 322 of the Companies Act, that a majority of the directors are shareholders of the company and members of the stock exchange, and that the directors have "unlimited liability" in the company. Under the amended rules, notified in the Gazette of India Extraordinary, the stock exchanges would admit these members on the recommendations of several financial institutions, including the Industrial Finance Corporation and the Industrial Development Bank of India

Rules framed for stock dealers-

The Securities and Exchange Board of India (SEBI) has framed rules to register and regulate stock dealers, share shoppes, and unauthorised stock exchanges under Section 12 of the SEBI Act. These rules are proposed with a view to redressing the grievances of investors in semi-urban and rural areas who have been experiencing difficulties in getting services for disposal of securities or consolidating odd lots. The regulations impose a statutory duty on stock dealers to deal only on a spot delivery basis and issue receipts in a specified form. Additionally, every applicant eligible for grant of a certificate must pay an initial fee of Rs 50,000 to keep the certificate in force. Stock dealers will have to submit information relating to their activities as and when required by SEBI.

Regulation of Scheduled Industry

A Select Committee has proposed a Central Advisory Council to advise the Government on development and regulation of scheduled industries. The revised Bill includes provisions to levy a cess on manufactured goods to fund the administration of the Act and a new clause has been inserted for safeguarding the interests of the consumers. The measure aims to balance industrial development with consumer protection.

Reviving cult of equity Management holds key

The improved and improving economic prospect has not had any impact on the stock market, which continues to present a picture of utter despondency. The cult of equity stands thoroughly discredited, as many relatively new issues once considered a rage now go abegging. While the state of the stock market is dominated by speculators, the capital market is influenced by financial institutions. More than anything else, gross mismanagement of companies and enormous cost overruns have undermined investor confidence. Although the link between the stock and capital markets is not as strong as often made out, the equity market must still play an important role in mobilizing national savings.

Reforms will change stock market operations

Stock brokers on India's 20 exchanges have initiated a dialogue with the Securities and Exchange Board of India (SEBI) following a spontaneous strike regarding quantum of registration fees to be charged by SEBI. While the broker community resists regulation, it is fairly certain that deregulation and liberalization in the economy will bring a drastic change in the way Indian brokers do their business. Currently, exchanges are riddled with problems like unbridled speculation and insider trading. SEBI requires substantial funds to monitor these activities, conduct research, and provide investor protection. Ultimately, the core of these reforms will be the stock exchanges themselves, as securities regulation must be tightened to maintain investor confidence.

Recognition sought for - Bombay Native Share and Stock Brokers' Association

The Bombay Native Share and Stock Brokers' Association has formally applied for recognition under the Bombay Securities Contracts Control Act, 1925. The Association has submitted rules for the regulation and control of transactions in securities other than ready delivery contracts for sanction by the Governor-in-Council. Membership is restricted to British subjects or natives of India resident in the Presidency for ten years, with strict solvency requirements to ensure the integrity of the exchange

Objectionable Practices On Stock Exchanges, DR. THOMAS RECOMMENDS-

A report by Dr. P.J. Thomas calls for the establishment of a National Investment Commission, modelled after the US SEC, to suppress objectionable practices on Indian stock exchanges. Identifying "violent fluctuations" caused by reckless speculation as a major evil, Thomas recommends strict regulation of blank transfers, the abolition of "kerb" trading, and the enforcement of compulsory margins. He argues that only an independent quasi-judicial authority can effectively police the market.