Regulations

SEBI exercises regulatory and supervisory control over the securities market by issuing the regulations, guidelines, and circulars to various market intermediaries and participants. This includes entities such as mutual funds, stock brokers, merchant bankers, depositories, depository participants, custodians, credit rating agencies, among others.

Read Articles

View All

Flexibility in Framework for Voluntary Delisting

Voluntary delisting refers to the process through which a listed company seeks to remove its equity shares from a recognized stock exchange, subject to regulatory safeguards that ensure fair treatment of its public shareholders. Since delisting deprives investors of future trading opportunities on the stock exchange, the regulatory framework has been progressively strengthened to ensure transparency, fair price discovery and an equitable exit mechanism. Beginning with administrative guidelines in 1998, the framework has evolved through expert committee recommendations, consultation papers, Board deliberations and regulatory amendments into a comprehensive principles-based regime under the SEBI (Delisting of Equity Shares) regulations.

Overview of SEBI Regulations for Registrars and Transfer Agents

The SEBI (Registrars to an Issue and Share Transfer Agents) Regulations, 1993 notified on May 31, 1993 have served as one of the important fundamental regulatory framework for the Indian securities market. With the technological developments, the way in which securities are issued, held, and transferred is now fundamentally different. Registrars to an Issue and Share Transfer Agents (RTAs) are key to this process. Further, the number of securities held in physical form has been going down consistently after the introduction of dematerialization of securities. It may be mentioned that the number of physical shareholding is less than 1% of the total holding as on March 31, 2025. Role of RTAs has further reduced in view of the fact that securities are issued only in dematerialized form. In response to this changing landscape, SEBI undertook a comprehensive review of RTA regulations, 1993 resulting in notification of SEBI (Registrars to an Issue and Share Transfer Agents) Regulations, 2025 on December 16, 2025.

D C Anjaria Committee on Review of SEBI Fee Structure for Stock Brokers

The fee structure for the brokers prescribed in the regulations was based on the recommendations made way back in 1992 by the R S Bhatt Committee. The recommendations of the Committee were based on the then level of brokerage earned by the brokers. Over the next decade, the market structure witnessed sea change, which coupled with fierce competition among brokers, has brought down the level of brokerage drastically. This necessitated a review of the fee structure for the stock brokers. Accordingly, on January 21, 2002, SEBI constituted a Committee under the Chairmanship of Mr. D. C. Anjaria to review the fee structure for the stock brokers. The Committee submitted its report during November 2003.

.png)

Watch Videos

View All

Evolution of Securities Market Regulations part 1

This video is the part 1 of the two-part series on regulations of securities market.

Evolution of Securities Market Regulations part 2

This video is the part 2 of the series showing evolution of securities market regulations in India.

Initiatives for Protection of Investors

The video gives a brief about the initiatives undertaken by SEBI for Investors protection

View Images

View All

A.D. Shroff’s Advice to Government

The Shroff Committee on "Finance for the Private Sector" has recommended that banks should proactively increase their investments in the shares and debentures of industrial concerns. The report urges a shift in attitude, suggesting that banks and indigenous bankers subscribe to special institutions like the Finance Corporations to accelerate the country's economic march. The committee emphasizes creating a spirit of partnership to meet the growing financial requirements of the private sector.

Malegam report to squeeze out a host of intermediaries

The recommendations of Malegam Committee appointed by SEBI are widely seen as a pointer towards disclosure norms in the Indian capital market moving towards international standards. But analysts expect that a strong concerted lobby by market intermediaries may develop against implementation of the report. The recommendations are aimed at making offer documents and prospectuses more transparent and investor friendly.

Gorwala Economy Committee

The Gorwala Economy Committee has submitted a report to the Hyderabad Government recommending drastic cuts to save Rs 3.6 crores annually. The proposals have sparked unrest among non-gazetted officers who face the brunt of the austerity measures.

Stock Exchange Reforms - a sharp critique of the Morrison Committee recommendations

A reader's letter to the editor argues that the Morrison Committee failed to grasp the real risk of the market regarding recommendations for government consent to close the exchange. The author contends that the government may commit an error of judgment in withholding sanction to close the market during bear raids, potentially demoralizing the entire market. While the committee suggests a system of margins, the author believes this may not prevent speculation and could create many complications. Instead, a better system for averting crisis is to vest brokers with lawful powers to close a client's business when the market is unfavourable. Such a change would impose a necessary check on initial transactions.

SEBI accepts Malegam panel report

In a major crackdown on low-quality public issues, the SEBI Board has accepted the Malegam Committee recommendations, effectively barring companies with a post-issue equity of less than Rs 5 crore from accessing the market directly. These firms must now route via the OTCEI or use market-making mechanisms. The new norms also enforce stricter disclosure standards in prospectuses, mandate the quantification of auditor qualifications, and introduce book building for large issues over Rs 100 crore

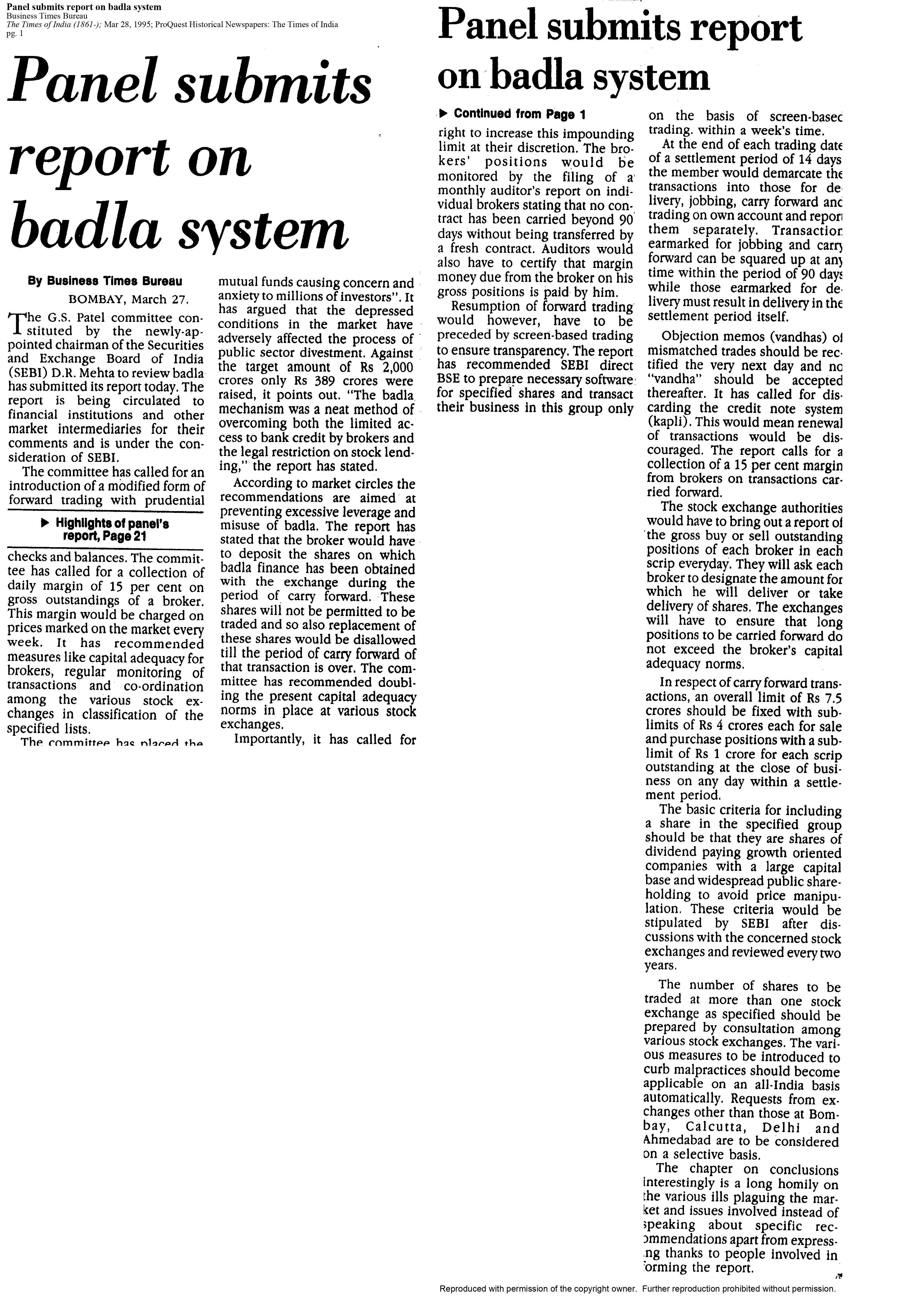

Panel submits report on badla system

The G.S. Patel committee, constituted by SEBI, has submitted its report calling for the introduction of a modified form of forward trading with prudential checks and balances. The committee recommended a daily margin of 15 per cent on gross outstandings of a broker and doubling the present capital adequacy norms. It noted that depressed market conditions, which saw a decline in prices of more than 1,00,000 crores, adversely affected public sector divestment. Resumption of forward trading would have to be preceded by screen-based trading to ensure transparency and prevent misuse.

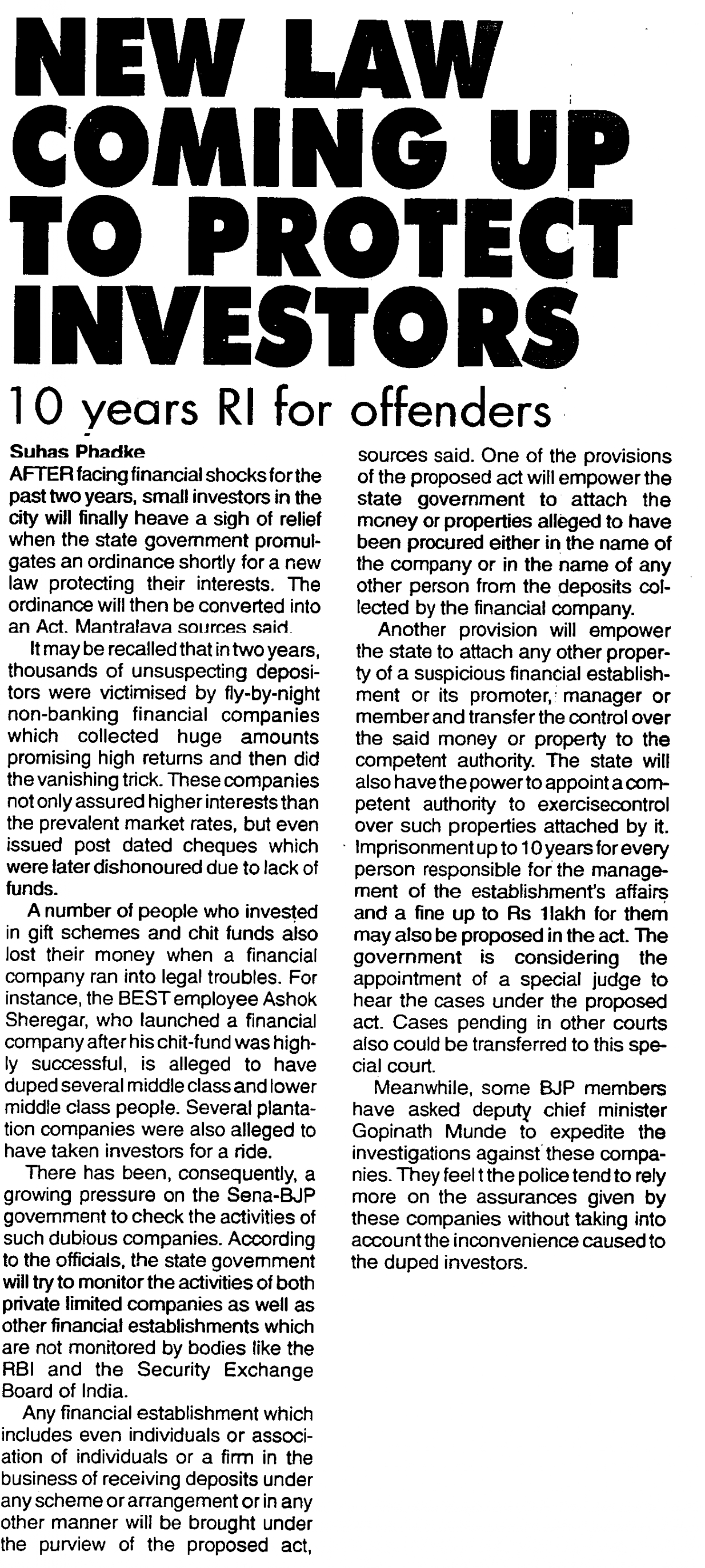

New Law Coming up to Protect Investors

The state government is set to promulgate an ordinance for a new law to protect small investors from non-banking financial companies (NBFCs) that vanish with deposits. The proposed act will empower authorities to attach properties of the company and its promoters to recover investors' money. With penalties including up to 10 years of imprisonment, the law aims to curb the schemes that have duped thousands.

Gupta panel submits draft norms for market making

The G.P. Gupta committee, appointed by SEBI, has submitted draft recommendations to introduce market-making for specific illiquid shares. The panel suggests a voluntary system where market-makers provide two-way quotes in the shares at regular intervals of 30 minutes with minimum depth of Rs 5,000 or one market lot, whichever is higher, aiming to inject liquidity into the secondary market. To ensure commitment, the committee proposes that registration be cancelled if a member fails to provide quotes for three consecutive days, while exchanges are tasked with prescribing capital adequacy norms.

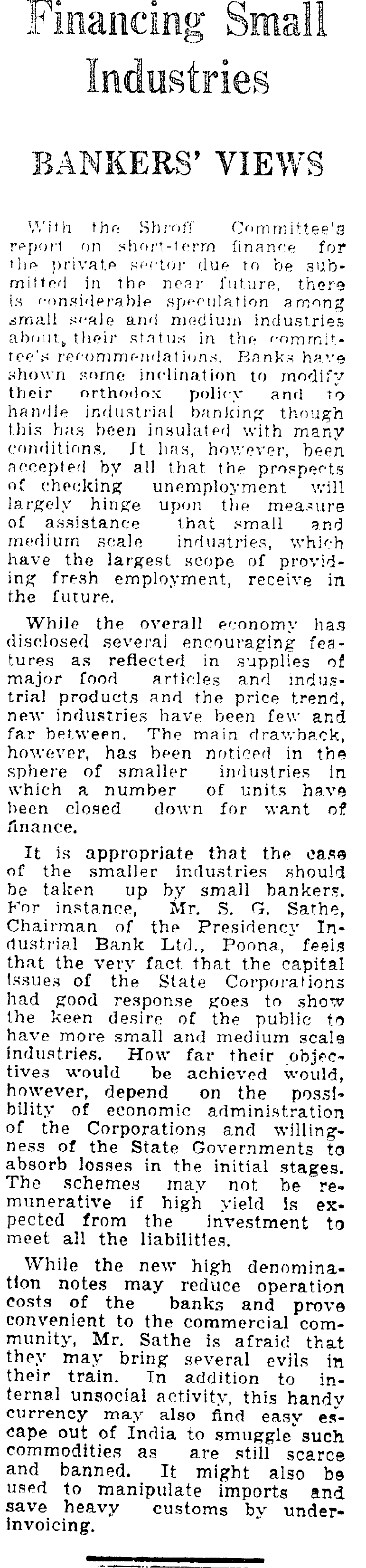

Financing Small Industries

With the Shroff Committee's report on short-term finance for the private sector due soon, there is speculation among small and medium industries regarding their status in the recommendations. Banks have shown some inclination to modify their orthodox policy towards industrial banking, but with many conditions. It is accepted that checking unemployment largely hinges on the assistance these industries receive, as they have the largest scope for providing fresh employment. While the overall economy shows encouraging features, new industries have been few, and many smaller units have closed down due to lack of finance. Mr. S. G. Sathe is afraid new high-denomination notes may bring several evils, including internal unsocial activity and easy escape out of India to smuggle scarce and banned commodities

Features of Report, recognised measures prevent gambling in a Stock Exchange

A reader, Jaya Raj, critiques the Stock Exchange Enquiry Committee's Report for being "innocuous" and lenient toward market manipulation. The letter argues that by failing to rigidly enforce the Rule of Margins, the Committee has offered an "easy alternative" that will not effectively curb gambling. The writer scoffs at the suggestion of Government-appointed directors as an ineffective check on speculation. However, the report is praised for some progressive steps, specifically the recommendation to abolish Blank Transfers and the demand for deposits from new members, which are seen as necessary sanitary measures for the exchange .