Brief Introduction of Equity Markets

Equity markets comprise of the electronic ecosystem and processes through which, investors buy and sell shares of publicly traded companies and also through which companies (listed and unlisted) raise capital from public/selected shareholders. Equity Shares, or commonly called as shares, represent a share of ownership in a company. An investor who invests in shares of a company is called a shareholder, and is entitled to receive all corporate benefits, like dividends, capital appreciation, bonus shares, etc of that company.

The primary function of equity market is to enable channelization of savings from investors who have money to those who need it. Equity markets also enable companies to be traded publicly and raise capital to grow their businesses, expand operations and create capital formation and jobs in the economy. The equity market constitutes two main segments:

Primary market - Unlisted /listed companies can access primary markets for raising capital through initial public offering, further public offering , rights issues, preferential allotments and qualified institutional placements. Pursuant to an IPO, company is listed at the stock exchange.

Secondary market - Buying or selling of shares of companies listed at stock exchanges happens under the domain of secondary markets. The process of buying or selling shares online in India has been made smooth and seamless, due to systematic functioning stock exchanges, clearing corporations and depositories , (collectively called Market Infrastructure Institutions-MIIs) and a host of intermediaries. In India, there are two main stock exchanges for equity (share) trading viz Bombay Stock Exchange (BSE) and National Stock Exchange (NSE). Presently (at the end of November 2023), there are about 5300 companies listed on BSE and about 2300 companies listed on NSE. At the end of November 2023, value of the outstanding shares listed (market cap), on an all-India basis, stood at Rs.341 lakh crore.

Over the years, equity markets have facilitated corporates, large and small, in raising resources and is an important avenue for long-term wealth creation for investors.

Read Articles

View All

Evolution of Rights Issue Framework

SEBI has progressively transformed the rights issue framework to make it a faster, simpler and more investor-friendly mode of capital raising while preserving the pre-emptive rights of existing shareholders. The reforms culminated in the 2025 amendments, which reduced the rights issue timeline to just 23 working days, introduced greater operational flexibility and strengthened transparency and investor protection.

The Journey from “Badla” to Derivatives

Badla, once a symbol of speculative fervour, faced numerous challenges and regulatory scrutiny throughout its journey in Indias stock markets. While it provided flexibility, it was also marred by manipulation and risks. Its eventual decline marked a shift toward more stringent regulations and a focus on investor protection, shaping the evolution of Indias financial landscape. The rise and fall of Badla in Indias stock markets reflect the complex interplay between market innovation, regulatory oversight, and investor behaviour. From its origins as a solution to liquidity challenges, Badla transformed into a tool for speculation, driving both market growth and instability. The Atlay and Morison Committees, along with SEBIs interventions, highlighted the need for balance in market dynamics. The regulatory journey, marked by periodic bans and reinstatements, underscores the challenges of managing a dynamic financial ecosystem. As Indias financial landscape continues to evolve, the legacy of Badla serves as a reminder of the importance of adaptive regulation and proactive oversight. While Badla may have faded into history, its impact on Indias stock market development remains a crucial chapter in the nations financial narrative. Investors, regulators, and market participants can draw valuable lessons from this historical journey, shaping a more resilient and transparent financial future for India.

Introduction of T+1 Rolling Settlement Cycle by Stock Exchanges

Moving from T+5 rolling settlement which was commenced in January 2000 in a phased manner starting with 10 scrips, SEBI in April 2002 introduced T+3 rolling settlement cycle. The settlement cycle of T+3 under the Rolling Settlement System was shortened further to T+2 rolling settlement, w.e.f. April 01, 2003. With the objectives of mitigating risk, enhancing liquidity and increasing the efficiency of the settlement process, flexibility has been provided to recognized stock exchanges (“SEs”) to offer either T+1 or T+2 settlement cycle, w.e.f. January 01, 2022. This move positioned India as one of the earliest adopters of the T+1 settlement cycle. Accordingly, the T+1 was introduced by the stock exchanges on February 25, 2022 for limited set of stocks, while complete transition took place on January 27, 2023.

Framework for issuance of Differential Voting Rights (DVR) shares

New technology firms that have asset-light models (relatively fewer capital assets compared to the value of their operations) generally prefer equity over debt capital, as raising equity on a periodic basis leads to the dilution of founder/promoter stakes. For these promoter-led firms, retaining the founder’s interest & control in the business is of great value and Differential Voting Rights (DVR) shares as a mode of capital raising can effectively address the concerns. Based on the report of the DVR Group and the feedback received on the consultation paper floated by SEBI in March 2019, the issuance of shares with superior voting rights (SR shares) has been introduced under SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018

Segregation and Monitoring of Collateral at Client Level

In order to further strengthen the mechanism of protection of client collateral from (i) misappropriation/ misuse by TM/ CM and (ii) default by TM/CM and/or other clients, SEBI introduced the framework for segregation and monitoring of client collateral to enable identification of collateral at the client level.

Bombay Stock Exchange Enquiry Committee (Atlay Committee)

The Committee was constituted by Government of Bombay in 1923 under the chairmanship Sir Wilfrid Atlay to enquire into the constitution, customs, rules, regulations and methods of business of the Native Share and Stock Brokers’ Association of Bombay with a view to protecting the investors and formulating future proposals. The Committee found that the Native Share and Stock Brokers’ Association of Bombay was a voluntary association with over 400 members, primarily focused on protecting member interests and providing a market for buying and selling stocks and securities, with rules and regulations regularly updated.

Evolution of Company Laws in India

This article explores the historical evolution and significance of Indian Companies Acts from 1850 to 2013 in shaping corporate governance and the securities market in India. It highlights key milestones in the development of company laws, such as limited liability, mandatory audits, financial disclosures and the establishment of regulatory bodies like SEBI. The article also discusses the impact of these acts on corporate governance practices, transparency, accountability, and investor protection. It emphasizes how these legal frameworks have facilitated economic growth and attracted investment, with iconic companies benefiting from the evolving regulatory environment. The Companies Act of 2013, with its modernization efforts, is seen as a turning point in promoting a transparent and investor-friendly corporate environment.

Introduction of Graded Surveillance Measures (GSM)

SEBI GSMs work as pre-emptive steps to reduce/check instances of market manipulation in identified scrips. GSMs are intended to deal with the abnormal increases in share prices of companies that are apparently not in line with their disclosed fundamentals or business models, particularly those with poor fundamentals.

Streamlining the Process of Rights Issue process and the dematerialized REs framework

SEBI laid down the detailed procedure of the improved Rights Issue process and the dematerialized REs framework.

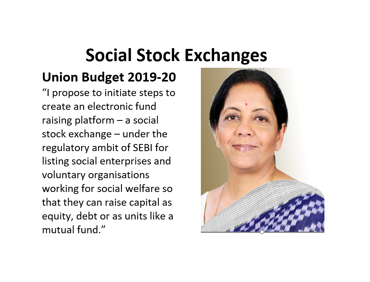

Operationalisation of Social Stock Exchange

In the Union Budget 2019-20, the creation of Social Stock Exchange (SSE) was proposed by the government, under the regulatory ambit of SEBI, for facilitating fund raising by social enterprises (SEs). The SEBI Board approved the creation of SSE on September 28, 2021, pursuant to public consultations and deliberations, and the recommendations of Working Group and Technical Group on SSE.

Watch Videos

View All

Evolution of equity investment cult in India

This video presents a brief on equity market investments in India

Evolution of Mutual Funds through numbers

This video gives presents the evolution of markets in India with the help of Data.

AIFs, REITs and INvITs

The video gives a brief about the emerging asset classes

Evolution of SAST Regulations, 2011

The video gives a brief account of SEBI (Substantial Acquisitions of Shares & Takeover Regulations), 2011 in India

View Images

View All

Reviving cult of equity Management holds key

The improved and improving economic prospect has not had any impact on the stock market, which continues to present a picture of utter despondency. The cult of equity stands thoroughly discredited, as many relatively new issues once considered a rage now go abegging. While the state of the stock market is dominated by speculators, the capital market is influenced by financial institutions. More than anything else, gross mismanagement of companies and enormous cost overruns have undermined investor confidence. Although the link between the stock and capital markets is not as strong as often made out, the equity market must still play an important role in mobilizing national savings.

Stock exchange reforms and cult of equity

The Union finance ministry has appointed a high-level committee to conduct a comprehensive review of the working of stock exchanges for the first time in 30 years. This initiative aims to ensure their smooth functioning and expand their activities to better mobilise private savings for the corporate sector. While the government has offered several concessions to increase the popularity of shares and debentures, the mushrooming of unregulated consultancy firms remains a concern for the merchant banking business. To ensure orderly growth, the government may consider approving an official list of merchant bankers, similar to approved security brokers. Ultimately, these reforms are considered necessary for the development of the capital market and the long-term cult of equity.

IPO Prospectus

The Vandex Manufacturing Company has issued a prospectus to raise Rs 2 lakhs to expand its shoe manufacturing business in Secunderabad and Bombay. Taking over the assets of Watts Bros. & Co., the company aims to mass-produce affordable footwear using machinery. The prospectus highlights the "unlimited" demand for factory-made shoes in India and projects a dividend of around 20%, appealing to investors to back a modernized leather industry.

Indian Rayon plans Euro issue

Indian Rayon & Industries is planning a Euro issue of Global Depository Receipts (GDRs) to raise $150 million for its massive expansion plans. The company, having reported a 60% jump in gross profit, is investing over Rs 900 crores in projects including a cement plant, a 18.5MW captive power plant and a 16.5MW co-generation captive power plant.

Craze for public issues by FERA companies

Public issues by companies diluting their foreign equity under the Foreign Exchange Regulations Act (FERA) are being preferred by investors. These issues have evoked good response in the past few months, as small investors have reaped good benefits and there are fairly good chances of such issues being quoted at a premium. Consequently, there is a craze for such issues amongst prospective investors. All the stock exchanges in the country have been directed that in the event of over subscription of a public issue, the basis of allotment should be finalised keeping in view that it is predominantly in favour of applicants in lower categories of 50 to 200 shares of the face value of Rs. 10 each. Such steps protect the interests of genuine small investors.

BSE public offering oversubscribed 51 times

In a stunning display of investor confidence, the initial public offering (IPO) of the BSE—Asia's oldest exchange—was oversubscribed more than 51 times. The offer, which saw the share price band set at Rs 805-806, attracted over 1 million applicants, with the HNI portion subscribed 159 times. The strong demand has pushed the grey market premium to Rs 160, driven by the bourse's brand value and its strategic foray into the GIFT City international finance space.

<h1>HTML</h1>

Testing Purpose

Flag off derivatives with index futures: SEBI panel

The secondary market advisory committee of the Securities and Exchange Board of India, in its meeting here on Monday, April 20, 1998 discussed the Dr. L. C. Gupta committee recommendations on derivatives trading and agreed that derivatives should be introduced in a phase manner, beginning with index future.

NSE launches new mid-cap index

The National Stock Exchange to launch the "Junior Nifty" mid-cap index, comprising 50 stocks with a base period of November 4, 1996. The Index having representation of companies with medium-sized capital in the Indian capital market, is expected to have high hedging effectiveness for portfolios with midcap companies and appropriate for index based derivatives.

Rolling settlement set to commence from January 10, 2000

Prior to introduction of rolling settlement in India, when account period settlement of trades was placed at 15 days interval, one of the shortcomings of the clearing and settlement process of the Indian stock markets was the absence of system to reduce counter-party risk. Managing this risk is essential for the safety and efficiency of the market. To ensure an effective clearing mechanism, the SEBI during 1997-98 had advised all stock exchanges (during this time, there were 22 stock exchanges in the country) to set up clearing houses and settle all transactions through the clearing house only and not directly between members, as was practiced earlier. The stock exchanges were also required to necessarily complete their settlements within seven days and to conduct the auction immediately i.e. not later than eighth day. Subsequently, this period was reduced to weekly cycles (5 days) and rolling settlements is a logical extension of further shortening of the trading and settlement cycles. Accordingly, for the first time, rolling settlement was introduced by the SEBI by making it optional for dematerialised shares on T+5 basis. Subsequently, SEBI set January 10, 2000 for commencement of rolling settlement in a phased manner, starting with ten scrips having sufficient liquidity with daily turnover of rupees one crore.