Article Repository

Rain gambling, or "Barsat ka Satta", originated in Rajasthan, where the Marwari community, facing perennial water scarcity, speculated on monsoon patterns. It spread to Calcutta (now known as Kolkata) in the 1800s, faced British opposition in Bombay (now known as Mumbai), and led to a court victory for Marwari rain gamblers. Despite protests, legislative amendments caused its decline and eventual ban in Calcutta by 1900. This unique chapter in gambling history reflects human adaptability amid monsoon unpredictability, serving as a nostalgic reminder of India's early weather derivatives.

“… 50 million sterling, if not more, of real wealth had been allowed to disappear like the baseless fabric of a vision, and how on the debris of such fabric the Bombay (now known as Mumbai) of today was re-built…”- DE Wacha, A Financial Chapter in the History of Bombay City. The American Civil War, which took place from 1861 to 1865, had a profound impact on global cotton supplies. Amidst the crisis, India emerged as a crucial alternative source of cotton for the textile mills of Europe. The Bombay Presidency, in particular, played a pivotal role in supplying cotton to meet this growing demand.

on Stock Exchanges.jpg)

The history of bank failures dates back to a few centuries but recorded ones are as far back as 17th century. In the early 20th century, the world's financial landscape underwent significant transformation. As nations braced themselves for the impending chaos of World War I, India's economy had to confront multiple challenges. One of the most significant economic events during this period was the series of domestic bank failures between 1913 and 1921, which left an indelible mark on Indian stock exchanges. A notable case during this period was that of a prominent member of the Native Share and Stock Brokers Association (earlier known as Bombay Stock Exchange and now BSE), Mr. Jahangir Byramji, who had a substantial holding in Manekji Petit Mill shares, was adjudicated as an insolvent.

The Great Depression was the deepest and longest economic downturn of the 20th century that affected most of the major economies of the world. India, being a colonial export-oriented economy, was also adversely impacted by the Great Depression, primarily due to a crash in commodity prices in domestic and international markets. Further, stocks plummeted on major Indian exchanges, taking cues from global turmoil. However, by 1932, normalcy was restored in international trade and manufacturing activity and there was a sizable recovery in India as well. The article delves into the events leading to the Wall Street crash of 1929, the subsequent global economic depression, and the impact of these events on the Indian economy.

SEBI, vide circular December 03, 1997, advised all stock exchanges to open or maintain at least one Investor Service Centre (ISC) for the benefit of the investors. Such centres are required to, inter alia, provide counselling services and certain basic minimum facilities to the investors. The major stock exchanges were allowed to open as many ISCs as required. Considering significant developments in the securities market, including technological advancements, the provisions related to ISC (Investor Service Centers) of stock exchanges were reviewed. To enhance outreach to investors nationwide, stock exchanges were advised to utilize existing ISCs at various locations and were further instructed to open additional ISCs as necessary, in accordance with SEBI's specifications. The minimum basic facilities to be provided at each ISC were also specified.

Today, BSE and NSE cater to investors across the length and breadth of the nation. In the mid-to-late 20th century, equity investors outside the metro cities sought to invest through stock exchanges located in their regions. Delhi Stock Exchange, incorporated in 1947, and Bangalore Stock Exchange, set up in 1963, were a few such examples. Subsequently, several other regional stock exchanges were established in places such as Bhubaneswar, Coimbatore, Guwahati, Jaipur, Magadh, Saurashtra, Uttar Pradesh, etc. However, technological advances changed the dynamics, and between 2000 and 2006, the turnover at the regional stock exchanges decreased significantly. In 2012, SEBI mandated a minimum annual trading turnover of Rs.1,000 crore for all exchanges. Since the regional exchanges could not meet the criteria, most of them exited the market by 2017.

SEBI took several policy initiatives with the objective of facilitating the exit process for non-operational stock exchanges.

To improve the ease of doing business and to offer ease and convenience for investors to lodge their complaints, SEBI launched “SEBI SCORES” mobile application. SEBI SCORES, which is available on both iOS and Android platforms, will help investors access SCORES at the convenience of a smart phone.

Limited Purpose Clearing Corporation (LPCC) has been set up for the purpose of clearing and settlement of corporate bond repo transactions and to develop an active repo market. Accordingly, SEBI vide circular dated February 02, 2022 pave the way for establishment of LPCC by AMCs of Mutual Funds. The LPCCs are expected to help improve liquidity in the underlying corporate bond market.

Limited Purpose Clearing Corporation (LPCC) has been set up for the purpose of clearing and settlement of corporate bond repo transactions and to develop an active repo market, SEBI Board, during September 2020, permitted the setting up of a Limited Purpose Clearing Corporation (LPCC). Accordingly, SEBI, vide circular dated February 02, 2022, pave the way for establishment of LPCC by AMCs of Mutual Funds. The LPCCs are expected to help improve liquidity in the underlying corporate bond market.

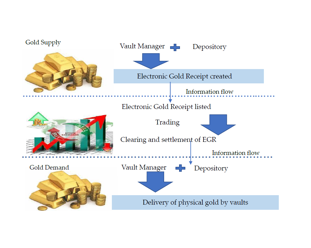

With the objective to put in place a risk management framework for Electronic Gold Receipts (EGR) segment, guidelines were issued by SEBI. The guidelines specified eligible collateral, applicable margins, reporting and verification framework of margins, penalty and shortfall management, norms relating to Settlement Guarantee Fund (SGF) etc. The risk management framework also provides guidelines for Clearing Corporation (CC) to have adequate capital buffer in form of margins and other collaterals, which are collected from members or is in the form of SGF to eliminate any kind of settlement risk and thus guaranteeing the settlement of trades which are executed on exchange platform.

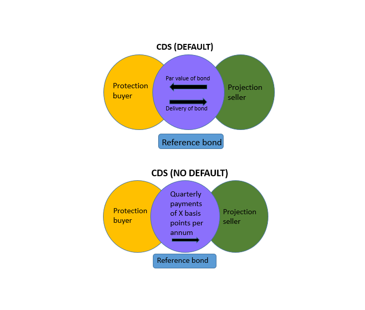

To provide greater investment flexibility to AIFs in managing credit risks and to facilitate deepening of the domestic corporate bond market, AIFs have been permitted to participate in Credit Default Swaps (CDS) not only as protection buyers but also as protection sellers, subject to conditions for risk management and mitigation.

SEBI, vide circular dated December 03, 1997, advised all stock exchanges to open or maintain at least one Investor Service Centre (ISC) for the benefit of the investors. Such centres are required to, inter alia, provide counselling services and provide certain basic minimum facilities to the investors. The major stock exchanges were allowed to open as many ISCs as required. Considering significant developments in the securities market, including technological advancements, the provisions related to ISC (Investor Service Centers) of stock exchanges were reviewed. To enhance outreach to investors nationwide, stock exchanges were advised to utilize existing ISCs at various locations and were further instructed to open additional ISCs as necessary, in accordance with SEBI's specifications. The minimum basic facilities to be provided at each ISC were also specified.

Considering the critical role played by Clearing Corporations, to manage outages on account of software failures, on the advice of SEBI, two leading CPs have implemented a two-way Software as a Service [SaaS] model. Under this first of its kind redundancy model, each CC has designed the risk management system for interoperable segments by deploying the software and related applications pertaining to risk management of another CC.

Following is the collection various Acts of Indian Securities Market. The acts may be downloaded from the link provided.

In view of the significant evolution of payment systems and sophisticated and robust technologies used by market infrastructure institutions (MIIs), SEBI decided to advance the clearing and settlement timelines to T+0 in equity cash segment, on optional basis. The Beta version of optional T+0 settlement cycle was introduced for a limited set of 25 scrips, and with a limited set of brokers.