Article Repository

This article explores the historical evolution and significance of Indian Companies Acts from 1850 to 2013 in shaping corporate governance and the securities market in India. It highlights key milestones in the development of company laws, such as limited liability, mandatory audits, financial disclosures and the establishment of regulatory bodies like SEBI. The article also discusses the impact of these acts on corporate governance practices, transparency, accountability, and investor protection. It emphasizes how these legal frameworks have facilitated economic growth and attracted investment, with iconic companies benefiting from the evolving regulatory environment. The Companies Act of 2013, with its modernization efforts, is seen as a turning point in promoting a transparent and investor-friendly corporate environment.

Equity markets comprise of the ecosystem and processes through which, investors buy and sell shares of publicly traded companies and where both listed and unlisted companies raise capital from public or selected shareholders. Equity Shares, or commonly called "shares" or "stocks", represent a portion of ownership in a company. An investor who purchases shares of a company becomes a shareholder, entitling them to a share of the company's profits and potential benefits, such as dividends, capital appreciation (increase in stock value), bonus shares and other corporate actions. .

The Committee was constituted by Government of Bombay in 1923 under the chairmanship Sir Wilfrid Atlay to enquire into the constitution, customs, rules, regulations and methods of business of the Native Share and Stock Brokers’ Association of Bombay with a view to protecting the investors and formulating future proposals. The Committee found that the Native Share and Stock Brokers’ Association of Bombay was a voluntary association with over 400 members, primarily focused on protecting member interests and providing a market for buying and selling stocks and securities, with rules and regulations regularly updated.

Badla, once a symbol of speculative fervour, faced numerous challenges and regulatory scrutiny throughout its journey in Indias stock markets. While it provided flexibility, it was also marred by manipulation and risks. Its eventual decline marked a shift toward more stringent regulations and a focus on investor protection, shaping the evolution of Indias financial landscape. The rise and fall of Badla in Indias stock markets reflect the complex interplay between market innovation, regulatory oversight, and investor behaviour. From its origins as a solution to liquidity challenges, Badla transformed into a tool for speculation, driving both market growth and instability. The Atlay and Morison Committees, along with SEBIs interventions, highlighted the need for balance in market dynamics. The regulatory journey, marked by periodic bans and reinstatements, underscores the challenges of managing a dynamic financial ecosystem. As Indias financial landscape continues to evolve, the legacy of Badla serves as a reminder of the importance of adaptive regulation and proactive oversight. While Badla may have faded into history, its impact on Indias stock market development remains a crucial chapter in the nations financial narrative. Investors, regulators, and market participants can draw valuable lessons from this historical journey, shaping a more resilient and transparent financial future for India.

In order to enhance efficiency ease of compliance and reduce cost, based on deliberations in the Secondary Market Advisory Committee of SEBI and discussions with stock exchanges and clearing corporations, it was decided that the promoters can also offer the shares to employees in OFS through the stock exchange mechanism, subject to certain conditions.

SEBI GSMs work as pre-emptive steps to reduce/check instances of market manipulation in identified scrips. GSMs are intended to deal with the abnormal increases in share prices of companies that are apparently not in line with their disclosed fundamentals or business models, particularly those with poor fundamentals.

SEBI, in its endeavour to provide an efficient mechanism for raising funds, has been continuously striving to streamline the process and methodologies associated with the public issue of securities. In this regard, SEBI, in 2018, introduced the use of Unified Payment Interface (UPI) as a payment mechanism with the facility of blocking funds (ASBA facility) for applications in public issues by retail individual investors, submitted through intermediaries.

New technology firms that have asset-light models (relatively fewer capital assets compared to the value of their operations) generally prefer equity over debt capital, as raising equity on a periodic basis leads to the dilution of founder/promoter stakes. For these promoter-led firms, retaining the founder’s interest & control in the business is of great value and Differential Voting Rights (DVR) shares as a mode of capital raising can effectively address the concerns. Based on the report of the DVR Group and the feedback received on the consultation paper floated by SEBI in March 2019, the issuance of shares with superior voting rights (SR shares) has been introduced under SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018

SEBI laid down the detailed procedure of the improved Rights Issue process and the dematerialized REs framework.

In order to further strengthen the mechanism of protection of client collateral from (i) misappropriation/ misuse by TM/ CM and (ii) default by TM/CM and/or other clients, SEBI introduced the framework for segregation and monitoring of client collateral to enable identification of collateral at the client level.

Moving from T+5 rolling settlement which was commenced in January 2000 in a phased manner starting with 10 scrips, SEBI in April 2002 introduced T+3 rolling settlement cycle. The settlement cycle of T+3 under the Rolling Settlement System was shortened further to T+2 rolling settlement, w.e.f. April 01, 2003. With the objectives of mitigating risk, enhancing liquidity and increasing the efficiency of the settlement process, flexibility has been provided to recognized stock exchanges (“SEs”) to offer either T+1 or T+2 settlement cycle, w.e.f. January 01, 2022. This move positioned India as one of the earliest adopters of the T+1 settlement cycle. Accordingly, the T+1 was introduced by the stock exchanges on February 25, 2022 for limited set of stocks, while complete transition took place on January 27, 2023.

In the Union Budget 2019-20, the creation of Social Stock Exchange (SSE) was proposed by the government, under the regulatory ambit of SEBI, for facilitating fund raising by social enterprises (SEs). The SEBI Board approved the creation of SSE on September 28, 2021, pursuant to public consultations and deliberations, and the recommendations of Working Group and Technical Group on SSE.

In order to enhance efficiency, ease of compliance and reduce cost based on deliberations in the Secondary Market Advisory Committee of SEBI and discussions with stock exchanges and clearing corporations, it has been decided that the promoters can also offer the shares to employees in OFS through the stock exchange mechanism, subject to certain conditions.

SEBI amended the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 vide the SEBI (Listing Obligations and Disclosure Requirements) (Second Amendment) Regulations, 2023, to introduce a "stricter timeline" for disclosure of material events or information by listed companies and criteria for determining the materiality of events. A few of these include: a. Quantifying the meaning of “material”, thereby limiting discretion with the listed entities, b. Requiring amendments to the Materiality Policy; c. Reducing timelines for disclosures; d. Mandatory verification of market rumours by the top 100 (250 from FY 24-25) listed entities; e. Broadening and shuffling of the events and information listed under Schedule III etc. The amendment regulations were applicable from July 14, 2023.

In its continuing endeavour to safeguard investors’ assets from misuse/ default by brokers, SEBI introduced a process for trading in secondary markets based on “blocked funds in investors’ bank account” instead of transferring the funds upfront to the broker. The mechanism harnesses public digitalisation infrastructure by integrating RBI approved Unified Payment Interface (UPI) mandate service (single block and multiple debits) with the secondary market trading and settlement process.

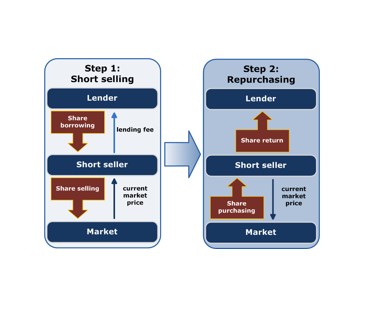

In order to provide a mechanism for borrowing of securities to enable settlement of securities sold short, SEBI has put in place a full-fledged securities lending and borrowing (SLB) scheme for all market participants in the Indian securities market under the overall framework of “Securities Lending Scheme, 1997” of SEBI. The Securities Lending Scheme was notified by SEBI on February 06, 1997. The guidelines for this facility of short selling and the framework for securities lending and borrowing have been specified in the Master Circular for Stock Exchanges and Clearing Corporations dated October 16, 2023. To enable the mechanism of short selling, the facility of securities lending and borrowing (SLB) scheme was put in place for all market participants under the overall framework of “Securities Lending Scheme, 1997” of SEBI. Further, SEBI issued a circular on the Broad Framework for Short Selling, modifying the Master Circular issued on October 16, 2023.

Curated Weblinks Data of Indian Securities Markets

In view of the challenges and limitations observed in buyback through the stock exchange route, SEBI (Buy-back of Securities) Regulations, 2018 was amended to dispense the same in a phased manner without disrupting the market.

In order to facilitate ease of doing business and reduce the cost of compliance for issuers accessing the primary market, the requirement to deposit 1% of the issue size available for subscription to the public with the designated stock exchange by the issuer company under regulation 38(1)of SEBI ICDR Regulations was dispensed with.